To own civilian ex lover-partners, it is vital to understand that becoming prior to now titled to the an effective Virtual assistant Loan cannot grant qualifications for Va Mortgage masters alone. Civilian ex-partners don’t use the veteran’s Va Mortgage entitlement to own upcoming purchases. Their capability in which to stay the home article-splitting up relies on refinancing possibilities and divorce or separation decree specifics.

Judge and Financial Information

Brand new implications out-of separation and divorce on the a great Va Loan suggest mindful courtroom and economic planning. Functions with it is talk to legal professionals focusing on nearest and dearest laws and possibly financial advisers understand brand new divorce’s effect on coming Va Loan entitlement and you will homeownership responsibilities. Such benefits can provide customized guidance, ensuring each party generate advised behavior about their assets and you can Va Financing experts.

Faqs regarding Virtual assistant Mortgage Companion Standards

Virtual assistant Financing are advanced, particularly if due to the character and you can perception regarding partners in the app procedure. So you’re able to describe well-known concerns and provide essential advice, check out your most often asked inquiries (FAQs) on the Va Loan lover conditions.

Zero, your wife doesn’t have to be on your Va Loan. Although not, together with your companion because the a co-debtor you are going to enhance the amount borrowed your qualify for, since their money is viewed as to compliment your credit strength. The decision to include a partner should be centered on a good comprehensive research of your combined financial situation and the possible feeling to your mortgage words.

Does my personal wife or husband’s credit rating apply at my personal Va Loan?

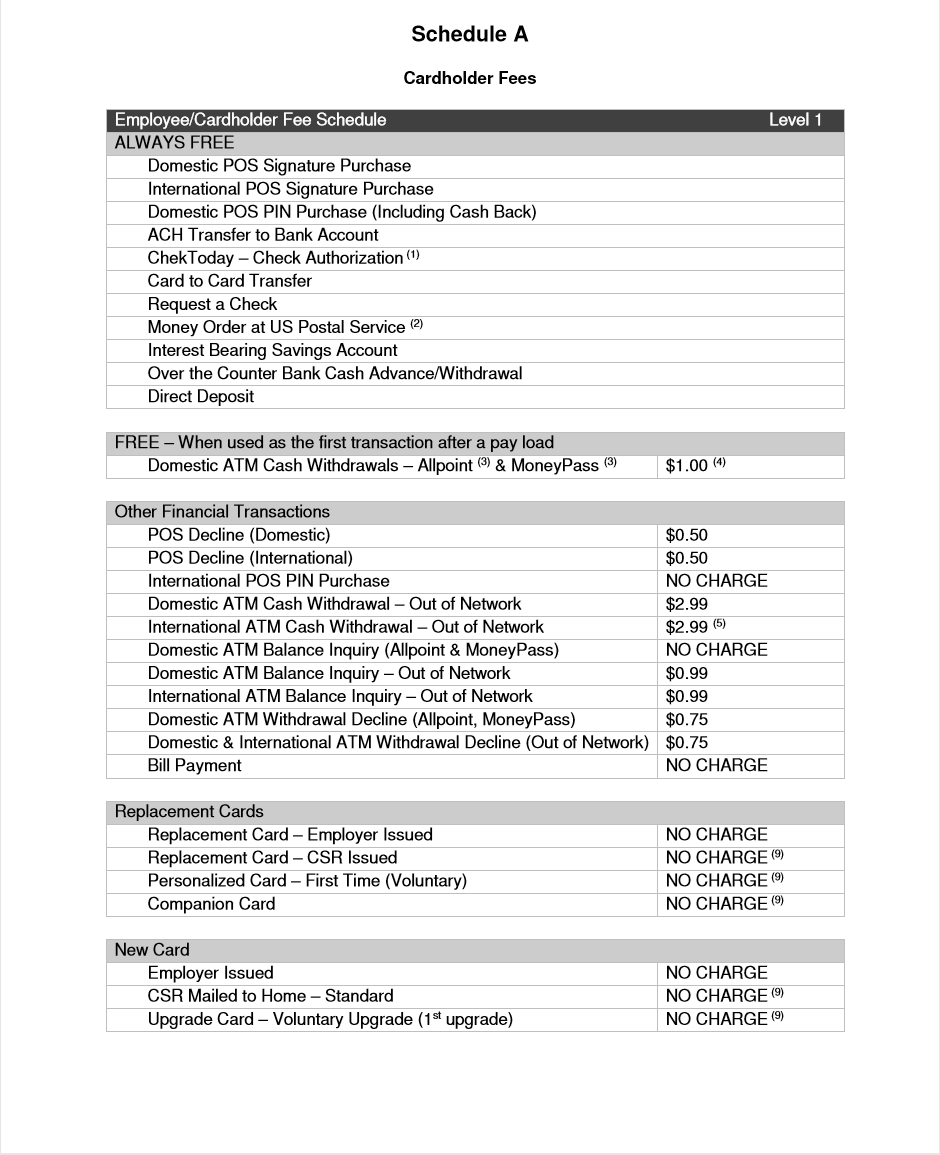

+WBlog.jpg)

Should your mate is not to the financing, the financial institution generally will not thought the credit score. Yet not, if you incorporate your spouse since the an excellent co-debtor, the credit history will in reality affect the mortgage. It attention may vary by the county and you can lender, particularly in society possessions states , in which a wife or husband’s bills and you will borrowing could be sensed, though they’re not good co-borrower.

Is also a non-companion get on the brand new title out of a Virtual assistant Mortgage?

Yes, a non-mate will be toward identity out-of a beneficial Virtual assistant Financing property, however, this may complicate the mortgage procedure. The newest Va allows for what’s labeled as shared funds for these points, in which a seasoned and you may a non-experienced (who isn’t new companion) should buy property to each other. However, the fresh new VA’s warranty merely pertains to the latest veteran’s part of the loan, and you may lenders might need new low-veteran and also make a deposit on the portion of the property.

Who will get on the newest term away from a good Va Financing?

When you take aside a great Virtual assistant financial, this new title range from the seasoned by yourself, the fresh new experienced in addition to their mate, or numerous veterans. When a veteran and a non-veteran (who isn’t a spouse) need to keep the term to one another, the loan are subject to various other conditions, such as for instance a down payment from the non-experienced co-borrower. New realities can vary of the financial and must getting discussed that have a beneficial Virtual assistant Loan professional.

How does divorce check this link right here now case perception a beneficial Va Loan?

Divorce case can rather impression an effective Va Loan, such as for example out of entitlement in addition to power to explore Va Mortgage gurus later. When your ex-spouse remains at home and on the original Virtual assistant Mortgage, this new veteran’s entitlement could be tied till the loan was refinanced or paid-in full. Court and you will financial suggestions is essential so you can browse these situations effectively.

Can an enduring spouse be eligible for an effective Virtual assistant Mortgage?

Yes, thriving partners from pros whom died in service otherwise out of solution-linked handicaps may be eligible for Virtual assistant Financing positives. They must fulfill specific conditions, instance not remarrying (or re also), as well as must obtain a certificate out of Qualifications to show its qualifications on experts.